The Sharpe Ratio

A well-known and often quoted measure of risk is the Sharpe ratio. Developed in 1966 by Stanford Finance Professor William F. Sharpe, it measures the desirability of an investment by dividing the average period return in excess of the risk-free rate by the standard deviation of the return generating process. In simple terms, it provides us with the number of additional units of return above the risk-free rate achieved for each additional unit of risk (as measured by volatility). This characteristic makes the Sharpe ratio an easy and commonly used statistic to measure the skill of a manager and can be interpreted as follows: SR >1 = lots of skill, SR 0.5-1= skilled, SR 0-0.5 = low skilled, SR = 0 = no skill and conversely for negative numbers. Although the Sharpe ratio can be an effective means of analysing investment performance, it has several shortcomings that one needs to be aware of and which I’ll discuss below. But before I do, here is the formula for calculating the Sharpe ratio:

(Mean Portfolio Return – Risk-Free Rate) / Standard Deviation of Portfolio Return

Sharpe Shortcomings

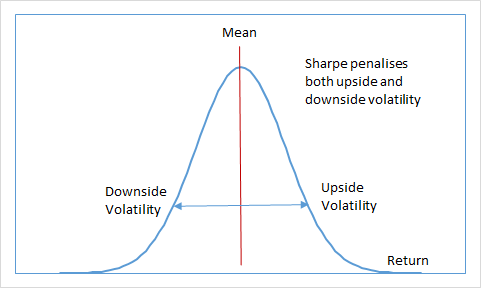

The most obvious and glaring flaw is the fact that the Sharpe ratio does not differentiate between upside (good) and downside (bad) volatility. Thus, a performance stream that experiences more positive outliers (a good thing for investors) will simultaneously experience elevated levels of volatility which will decrease the Sharpe ratio. This means that one can improve the Sharpe ratio for strategies that exhibit a positive skew in their return distribution (many small losses with large infrequent gains), for instance trend following strategies, by simply removing some of the positive returns, which is nonsensical because investors generally welcome large positive returns.

On the flipside, strategies with a negative skew in their return distribution (many small gains with large infrequent losses), for instance option selling strategies, are much riskier than the Sharpe ratio would have us believe. They often exhibit very high Sharpe ratios while they are “working” because they tend to produce consistent small returns that are punctuated by rare but painful negative returns.

The reason for the shortcomings discussed above can be attributed to the fact that the Sharpe ratio assumes a normal distribution in returns. Although strategy and market returns can resemble that of a normal distribution, they generally are not; if they were then we would expect some of the market moves we’ve experienced within the last decade to occur once in a blue moon, but they evidently do not. This is the result of the phenomena referred to as “fat tails”, or the market’s higher probability of realising more extreme returns than one would expect from a normal distribution. This, in and of itself, is reason enough to be dubious of blindly evaluating a manager or strategy’s performance based on a Sharpe ratio without an understanding of exactly how the returns are made.

One also needs to place the reason for the Sharpe ratio’s initial development into perspective. It was conceived as a measure for comparing mutual funds, not as a comprehensive risk/reward measure. Mutual funds are a very specific type of investment vehicle that represent an unleveraged investment in a portfolio of stocks. Thus, a comparison of mutual funds in the 60’s, when the Sharpe ratio was developed, was one between investments in the same markets and with the same basic investment style. Moreover, mutual funds at the time held long-term positions in a portfolio of stocks. They did not have a significant timing or trading component and differed from each other only in their portfolio selection and diversification strategies. The Sharpe ratio therefore was an effective measure to compare mutual funds when it was first developed. It is however not a sufficient measure for comparing alternative investments such as many hedge funds because they differ from unleveraged portfolios in material ways. For one thing, many hedge funds employ short-term trading strategies and leverage to enhance returns, which means when things go wrong money can be lost at a far greater rate. Moreover, they often do not provide the same level of internal diversification nor have lengthy track records.

Investors that do not understand the difference between long-term buy-and-hold investing and trading, often incorrectly measure risk as smoothness in returns with the Sharpe ratio. Smoothness does not equal risk. In fact, there is often an inverse relationship between smoothness and risk – very risky investments can offer smooth returns for a limited period. One need only consider the implosion of Long-Term Capital Management which provided very smooth and consistent returns (excellent Sharpe ratio) before being caught in the Russian default on bonds which created a financial crisis.

The strategies that we employ in QuantLab would be categorised as alternative in nature and do not mimic typical mutual funds. Therefore, the Sharpe ratio is not the most suitable measure to assess our performance. So, let’s examine a couple of alternatives to the Sharpe ratio.

The Sortino Ratio

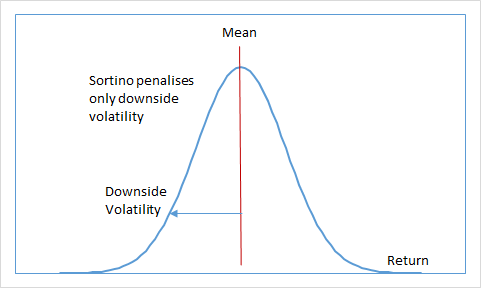

The Sortino ratio is like the Sharpe ratio but differs in that it takes account of the downside deviation of the investment as opposed to the standard deviation – i.e., only those returns falling below a specific target, for instance a benchmark. Formula:

(Mean Portfolio Return – Risk-Free Rate) / Standard Deviation of Negative Portfolio Returns

The Sortino ratio in effect removes the Sharpe ratio’s penalty on positive returns and focuses instead on the risk that concerns investors the most, which is volatility associated with negative returns. It is interesting to note that even Nobel laureate Harry Markowitz, when he developed Modern Portfolio Theory (MPT) in 1959, recognized that because only downside deviation is relevant to investors, using it to measure risk would be more appropriate than using standard deviation.

We can see the effects of removing the penalty on positive outliers with the Sortino ratio by examining our live performance in QuantLab, which to date exhibits a strong positive skew – we’ve enjoyed several large positive outliers – so the Sharpe ratio unfairly penalises our performance. In fact, if we remove the effect of positive volatility (good for investors), QuantLab’s risk-adjusted performance improves from 1.11 (Sharpe) to 1.85 (Sortino). However, since the return stream of QuantLab is asymmetric, that is it displays skew and is not symmetric around the mean, the standard deviation is not an adequate risk measure (as discussed above). Although the Sortino ratio improves on the Sharpe ratio for performance profiles that exhibit positive skew, it still suffers from the flawed assumption that returns are normally distributed, which is required when using the standard deviation to measure risk.

There is however an alternative risk/reward measure free of the shortcomings discussed above which I personally prefer to use when evaluating performance. I’ll explore this measure next.

The MAR Ratio

In an absolute sense, the most critical risk measure from an investors perspective is maximum drawdown because it measures the worst losing run during a strategy’s performance. A pragmatic approach then to measuring risk/reward is to determine how well we’re compensated for assuming the risk associated with drawdown. This is precisely what the MAR ratio achieves. It was developed by Managed Accounts Reports (LLC), which aptly reports on the performance of hedge funds. The ratio is simply the compounded return divided by the maximum drawdown. Provided we have a large enough sample, the MAR ratio is a quick and easy to use direct measure of risk/reward; It tells you how well you’re being compensated for having to risk your capital though the worst losses. The formula follows:

CAGR / Max DD

l find this ratio immensely useful. It’s simple, does not rely on flawed assumptions about market return distributions such as standard deviation, which is used in both the Sharpe and Sortino ratios, and it measures what’s important to investors: the number of units of return delivered for every unit of direct risk (maximum drawdown) assumed. When we use this metric to measure our live performance to date we find that QuantLab has delievered three units of return for every unit of risk, that is, our live MAR ratio is currently 3.

The MAR ratio is a transparent and direct measure of risk and reward that is impossible to manipulate (the Sharpe and Sortino ratios can be manipulated higher in several devious ways) and is thus my preferred measure of risk-adjusted performance when evaluating strategies.

Conclusion

We all have unique return expectations and tolerance for pain. For this reason, there is no single measure that appeals universally to everyone. In my personal trading, I analyse the MAR ratio, maximum drawdown, overall return and like to keep an eye on the smoothness in which returns are generated by examining the Coefficient of Variation, Sharpe and Sortino ratios. Keep in mind that regardless of the statistic you use, they are good estimates at best. Therefore, one can never be too conservative when analysing past performance. Given a long enough timeline, every strategy will exceed its maximum drawdown. This is a harsh reality that we as traders need to accept and prepare for, so it’s a good idea to be suspicious of any statistic and ensure we have buffers built into our expectations to handle new extremes that will likely be posted in the future.

As always, I welcome your thoughts and suggestions.

Happy Trading,

PJ

4 comments On Alternative to the Sharpe Ratio

What do you think of Van Tharp’s SQN (Expectancy / SD of avg loss ie T-score) it combines both Sortino (because R is based on ave loss) and inverse of CV ratio? Do you use it?

I like it since it includes all the factors that good traders should be looking to maximise i.e. the number of trade opportunities, the average P&L and the volatility of the return stream. That said, I find it valuable to view the same statistics individually in their component parts. For instance, a strategy with a higher trade count will produce a relatively higher SQN, but for various reasons, I may still prefer the lower trade count strategy. I would always use SQN alongside other metrics – I think it’s difficult to bring performance down to a single number without understanding the component parts. This is especially true when building a portfolio made up of many strategies where the diversification benefits a particular strategy adds to the portfolio becomes much more important than a single performance number I.e. it may make a lot more sense to add a strategy with a lower SQN purely based on the diversification it adds to a portfolio. I guess I use more art than science when evaluating strategy performance.

What are your thoughts about time frames – daily, monthly, annually- when calculating / reporting these metrics?

It depends on what you’re trying to measure from an investors perspective. Since we can measure returns and volatility in smaller time-frames, the calculations can be done for any period you chose (even seconds/minutes if you’re so inclined). If you are an investor that monitors a portfolio on a monthly basis and don’t care about the daily equity swings, then it would make sense to go with monthly data. The same goes for daily/quarterly/semi-annually/annually. It’s a matter of how much volatility you can stomach and in what time-frame. The industry standard is monthly because generally hedge funds report returns monthly.