I’ve seen studies in the past that suggest that there’s an optimal day of the week to trade. One well know trader in particular, Larry Williams (famous for trading $10K to $1.1 mill in a single year with real funds in a global trading competition) , discusses “best-day-of-the-week” as a strategy overlay in his excellent book “Long term secrets to short-term trading”. I’m personally very sceptical of such an approach because it is susceptible to data mining bias I.e. the perceived edge is likely due to chance as opposed to economically sound logic. It’s important to bear in mind when testing a strategy: correlation does not always imply causation. In other words, if Monday’s appear to be the most profitable day of the week, it does not necessarily follow that Monday’s are the cause of higher returns – the relationship may exist due to pure chance alone. So in today’s blog I’ll attempt to prove or disprove the above theory and determine whether this simple overlay provides statistically significant.

Testing the Theory

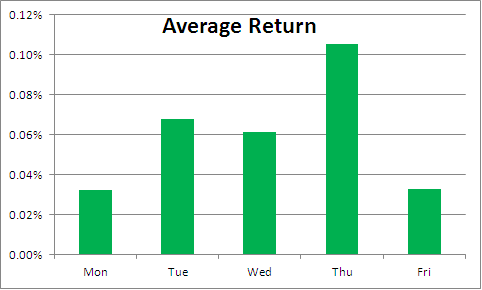

The first test I ran looked at the daily returns of liquid equities listed on the JSE for each day of the week, namely Monday through Friday, since 2003. I then ran a similar test for the percentage of winners. Both tests can be viewed graphically below:

The first bar chart represents the average trade return for each day of the week. The chart suggests that Monday’s and Friday’s underperform (Monday hangover and Friday weekend excitement perhaps?), while Tuesday through Thursday outperform, with Thursday being the best performing day of the week. The second chart represents the percentage of winners and presents a mixed bag of results: we find confirmation of the prior chart on Thursday and Friday, but see contradictions on Monday and Wednesday. This suggests to me that the results of the first chart may be due to chance, or the result of a small number of outliers that have skewed the results higher and which are unlikely to repeat in the future. Let’s see if we can prove our suspicions further.

Digging Deeper

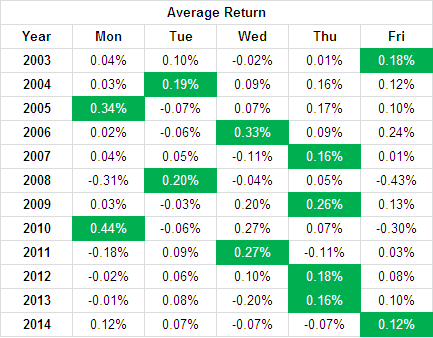

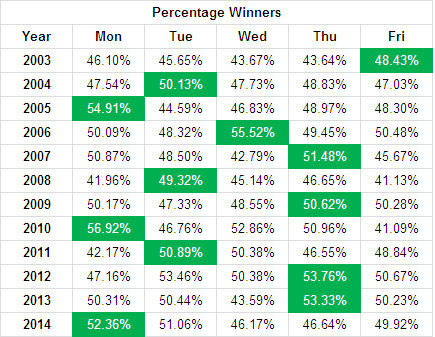

If the data above are statistically significant we’d expect to see similar results for each individual year. To investigate this I ran precisely the same tests as above for each year on a standalone basis. My results are presented below – green cells indicate the best day of the week for the year in question.

In the first table we find that Mon, Tue, Wed and Fri performed the best in 2 of the 12 years (a perfectly even spread), while Thursday performed the best in 4 of the 12 years. In the second table we find that Mon and Tue exhibited the highest winning percentage in 3 of the 12 years, Wed and Fri in 1 of the 12 years and Thursday in 4 of the 12 years. The even spread and random nature of the data confirms our suspicions above: “Best-day-of-the-week” does not appear to be a real phenomenon.

Conclusion

Although we find some indication that Thursday’s tend to outperform in the data above, the sample is too small and the evidence too weak to provide statistical significance. Therefore, the anomaly observed in the data is highly likely to be the result of randomness or chance as opposed to some underlying and exploitable cause. We can thus conclude that there is no significant evidence that supports the “best-day-of-the-week” theory on the JSE. Unless you trade your portfolio on chance, there’s no value to this overlay.

Happy Trading,

PJ