Before we discuss methods to exploit the tendency for the stock market to rise during month end, I wanted to share the performance of simply implementing the strategy in its raw form against its inverse. The results are rather impressive.

EOM Strategy vs EOM Inverse Strategy Performance

For the test I used the following rules:

Universe: JSE listed and delisted equities since 2003

Liquidity Filter: HHV (High – Low, over 100 days) > 0 I.e. the stock has traded every day for the past 100 days

EOM Entry: Day of month >= 24th of the month, enter at close

EOM Exit: It is the last day of the month, exit at close

EOM Inverse Entry: It is the last day of the month, enter at close

EOM Inverse Exit: Day of month >= 24th of the month, exit at close

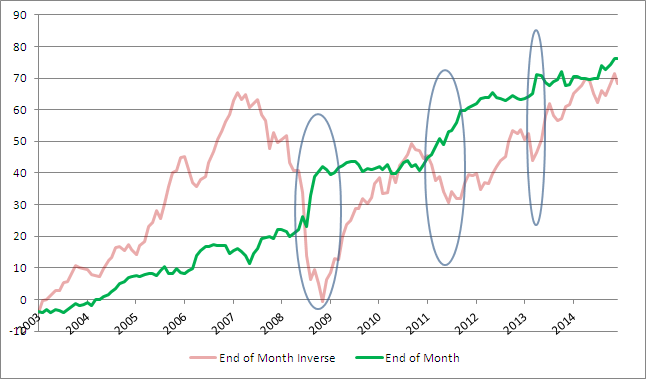

The performance table and charts below clearly emphasize the significance of this tendency; the EOM strategy outperformed its inverse with far less volatility, risk and time in the market. Its risk-adjusted measure (AV monthly return / monthly StD) exceeds its inverse by a factor of 2.23. That’s remarkable considering the strategy is only invested for roughly five days every month, as opposed to 25 days for its inverse.

What’s even more striking is the fact that the EOM tendency appears to be more pronounced during market downturns, as seen in the dramatic rise in cumulative returns during the financial crisis and other major sell-offs. Note also the non-correlation between the EOM strategy and its inverse – the EOM strategy’s performance tends to improve when the inverse performs poorly and vice versa (blue ovals on chart). This suggests to me that a larger portion of funds find their way to the markets during month end when performance for the month in question is negative, or when performance in general is deteriorating. This approach is typical of long-term deep value contrarian money managers, such as Alan Gray, who seek out fundamentally sound companies that are trading below intrinsic value, or in other words, companies whose stock prices are experiencing weakness. They then buy those companies in anticipation of long-term mean reversion to intrinsic value, pushing prices higher during the final five days.

As an aside, it would be interesting to see the results of overlaying a couple of simple fundamental filters to the entry condition to restrict trading in fundamentally sound stocks.

EOM Strategies

There are literally an unlimited number of ways one could exploit month end seasonality. I’m going to discuss some obvious ones here and leave the rest to your imagination. We’ll start with long-term strategies.

Rand-cost averaging

Rand-cost averaging is the practice of investing the same amount of money at regular intervals, usually monthly. If you currently allocate capital to the markets once a month then the best time to do so is between the 24th and the last day of the month. Setup an automatic transfer that is executed during this period. For instance, buy an equal rand value of the STX40 ETF during the final five days of each month, preferably on the 24th. This approach should improve your average entry price over the long-term.

To further improve performance, only make the allocation if the market is down for the month (as discussed above). I haven’t displayed the test data here, but risk-adjusted returns improve with this approach.

Retirement Withdrawals

Perhaps you’re in retirement and part of your income derives from selling enough of your stock funds each month in order to withdraw R5000. Wait until the favourable period has run its course; sell your shares on the last trading day of each month. Over the long-term, you’ll get a slightly better average price.

Let’s have a look at a couple of short-term ideas.

Mean Reversion

One could employ a simple mean reversion strategy and restrict its trading to the final five days of the month. My testing shows that this approach further improves risk-adjusted returns. One method involves using either the Relative Strength Index or Stochastics to uncover oversold stocks during month end. These could be bought and held for five days. One could also include a profit stop to increase win rates and mitigate volatility. This method will naturally decrease activity for the mean reversion strategy, but one could perhaps trade at lower levels of risk outside the month end and increase risk slightly during the turn of the month to capitalise on the monthly seasonality.

Momentum

What about creating some form of relative strength model that seeks exposure to the best performing stocks relative to their peers. One could run the model monthly and adjust portfolio holdings on the 24th of each month. Laggards would be removed and replaced with leaders. Making the changes just before the month end rally should slightly boost portfolio returns.

Conclusion

Remember, these patterns aren’t perfect. The seasonality studies reflect “averages.” By definition, an average finds the middle ground (and therefore hides the extremes). So don’t expect the favourable period to lead to higher prices every month.

As J.P. Morgan famously said, the only thing we know for sure about next month’s market is that “stocks will fluctuate.” Seasonality should be used only as one piece of an overall decision-making process.

Happy Trading,

PJ