After my blog last week on ANG the stock rose dramatically on an intraday basis, almost 9%! Many of our clients with long positions in the stock managed to close out near the highs, recouping most of their losses. I had someone ask what I thought caused the spike higher, to which I responded “raw emotion”. Traders that went short the bad news were squeezed out of their positions resulting in frenzied buying that temporarily pushed price to extremes. By the market close the stock had lost most of its gains and basically closed near its open. Efficient markets? I doubted! And on that note, I’d like to share an excerpt of a study I did this past week.

Evidence of Market Inefficiency

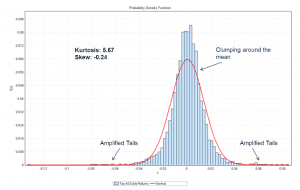

Analysing the daily returns of the JSE Top 40 index since 1995 we find that they do not follow a normal distribution – one which is expected of a random series of data. Our study in fact generated a kurtosis value of 5.6, which implies that price follows a leptokurtic distribution in the short-term. That is, prices tends to cluster around the mean more than suggested by a random distribution. Furthermore, the distribution exhibits amplified tails, or an increased probability of extreme events. In layman terms the market has a tendency to revert to the mean (clustering around the mean) as well as display powerful and sustainable trends (amplified tails) from time to time. These findings are diametrically opposed to theories of random market behaviour and efficient market hypothesis.

Our study validates what technical analysts have known for well over a hundred years: the market can be successfully traded for profit by employing either a trend following or mean reversion approach.

Mean reversion: attempts to capitalise on price reversions as seen in the clustering of price around the average price. Technicians employ tools such as Wilder’s Relative Strength Index or Stochastics.

Trend following: attempts to capitalise on price trends as seen in the amplified tails by buying highs and selling even higher. Technicians employ tools such as moving averages and price breakouts.

Mean Reversion

The market tends to be range bound around 70% to 80% of the time – as seen in the clustering around the average price – resulting in mean reversion being a more prevalent phenomenon than price trends. Therefore, strategies designed to exploit mean reversion typically enjoy high win rates, low drawdowns, quick recoveries and smooth equity curves. These are very desirable strategy attributes that led to my intensive research within this approach. However, there is one caveat. Mean reversion requires traders to fade mass psychology – buying when the majority are selling and selling when the majority are buying – and therefore poses considerable implementation risk. Without a well-tested mechanical approach traders can easily become victim to the very emotion they’re attempting to exploit. In order to protect from emotional bias, strategies need to be automated to the largest extent possible. Furthermore, tail risk, or the risk that price matures into a powerful trend without the expected reversion, needs to be carefully controlled.

I’ve spent the past 10 years researching mean reversion. My research has led me down many interesting rabbit holes, most of which were fruitless, but valuable nonetheless. My success came when I began to control tail risk and automate the trade process. QuantLab is the fruit of my labour.

Happy Trading,

PJ

2 comments On Is the JSE Efficient?

It would be interesting to analyse sectors or asset classes to understand their kurtosis in order to select a trading methodology. For example, real estate (with a kurtosis of 8.75) and High Yield US bonds (8.63) are high risk investments suitable for reversion to mean while Investment grade US bonds (1.06) and Small cap US stocks (1.08) may be more suitable for trend following? What methodology is most suitable for a mesokurtosis profile such as Small cap US stocks?

Great question. So I’ve done some research around this but in a more simplified fashion. Instead of measuring kurtosis directly, I developed an algorithm that measures the success of mean reversion on a given price series over a predefined look-back period. You could however use any number of methods, for instance a simple oscillator such as stochastics would also work. I was specifically interested in the win rate and average payoff and used these metrics as a high level binary filter for my mean reversion strategy i.e. if mean reversion is currently working (as determined by recent win rates and payoff), then turn on the strategy, otherwise turn off. I observed some impressive performance improvements. I did not test the reverse however i.e. if mean reversion is not working then deploy a trend following approach, but I imagine this is worthy of some investigation. As for mesokurtic, I’m not sure, but I’m guessing simply buying market exposure in a diversified manner may be a good bet.