In their excellent paper, Cole Wilcox and Eric Crittenden explore whether or not trend following strategies can achieve alpha when applied to the stock market. The vast majority of funds that operate trend following type strategies focus in the commodity and forex markets, where long-term sustainable trends driven by economic factors are more likely to unfold. Indeed, one of the most successful and famous groups of traders, the turtles, attained their success by applying a trend following approach to the commodity markets. The equity markets on the other hand have fewer success stories when it comes to trend following, and most professionals believe the equity markets are better traded using mean reversion strategies. My research, for the most part, confirms this to be true. However, by combining a mean reversion entry with a trend following exit (A technique I employ at www.quantlab.co.za) one can greatly improve the overall performance of trend following. But alas, I’m diverging. Today I want to focus on whether or not trend following is a worthwhile endeavour in the equity markets, and I’ll begin by taking my cue from the paper mentioned above – you can read the paper here. I’ve used the exact same entry and exit conditions discussed in the paper, but for your benefit I’ve summarised them briefly below.

Universe: The entire listed and delisted JSE equities I.e. survivorship bias free

Test Period: 2000 to the present

Liquidity filter: Stock price above R5 with an average daily volume of 250 000 shares

Entry Trigger: Stock makes new closing all time high

Entry Price: The opening price tomorrow

Initial Stop: 10 * ATR(40) from the entry price

Trailing Stop: 10 * ATR(40) from the most recent price

Position Sizing Algo: Fixed Percent Risk – 2% per trade

Broker Fees: 0.5%

Trend following is the epitome of the age old trader’s adage “Let your profits run and cut your losses short”. Trend following strategies typically hold winning trades for longer than losing trades and generate positive average returns from winners that far exceed those from losers. Below is an illustration of a notable winning trade in SBK.

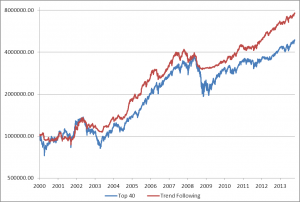

So how did trend following perform? Compared with the JSE Top 40 index trend following outperforms generating 14.54% compounded annual growth rate compared with the Top 40’s 11.12%. I’ve included an equity chart below contrasting the performance assuming a starting account of R1 million. My findings confirm the work of Cole and Eric and confirm the validity of trend following. In the long run, and with a huge dose of discipline and perseverance, one is likely to generate superior returns with a quantified trend following strategy. However, it’s important to note, that despite these results much additional work still needs to be done. Some of the things that need to be addressed are mentioned in the research paper, but suffice it to say that risk at portfolio level needs to be carefully considered.

In the next few months QuantLab will release a number of quantified trend following strategies to complement our current mean reversion strategies. Traders will be able to access all the past performance related to each strategy, rank strategies across countless metrics, build and test portfolios as well as execute the daily signals related to a strategy in a few simple mouse clicks.

Happy Trading,

PJ