Last year Rowan spoke about the importance of consistency in portfolio construction and today I’d like to expand on the concept a little. There are a number of reasons why consistency is important: 1) our performance pegged pricing structure is based on consistency 2) it’s psychologically easier to trade consistent portfolios 3) consistent portfolios enjoy quick recoveries from drawdown and lower maximum drawdown’s and 4) you’re more likely to achieve the backtested annual return in any given year for a consistent portfolio. In this post I’m going to discuss how we measure consistency, analyse real client performance alongside consistency and provide you with a simple formula to predict your annual return interval.

First let’s explore how we measure consistency in QuantLab. There are a number of ways to measure consistency in performance, we decided to use the Coefficient of Variation of monthly returns which we refer to as the CV ratio. The CV ratio is simply a strategy’s volatility divided by its return:

Monthly Standard Deviation / Average Monthly Return

From the above formula it’s plain to see that as risk, measured by the standard deviation, increases so too does the CV ratio. Therefore, lower CV ratios are preferable to higher CV ratios, or said another way the lower the CV ratio, the better your risk-return tradeoff. When deciding between two strategies with the same CAGR, it’s always optimal to choose the one with the lower CV ratio.

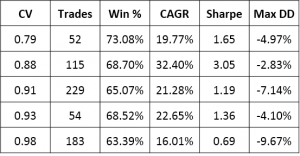

To emphasise the importance of the CV ratio in strategy selection, I’m going to share the live performance of five of our client’s portfolios ranked by the CV ratio in the table below.

By analysing the table you’ll find that the portfolio with the highest CV ratio is associated with the lowest CAGR and the worst maximum drawdown. However, the backtested CAGR of this particular portfolio is very high, it’s precisely 70.06%. So why then is this portfolio performing far below expectations? Well one of the reasons is the high CV ratio, or high volatility associated with the CAGR. High CV portfolios exhibit what I refer to as lumpy annual returns. In other words, some years deliver exceptional returns while others perform below average. This type of performance can be difficult to weather psychologically because one has high annual return expectations derived from backtesting that are often missed due to the high volatility in the return stream.

As mentioned above, portfolios with low CV ratios are more likely to achieve their backtested annual returns, or they display narrower return intervals. To demonstrate this I’m going to apply a simple statistical confidence interval to two strategies with similar CAGR’s but different CV ratios. The rule is known as the 68-95-99.7 rule and it measures the percentage of observations that lie within a band of one, two or three standard deviations around the mean. Below I’ve included the two strategies and their respective statistics.

For the band width I included the 95% rule i.e. we can be confident that 95% of annual return values fall within two standard deviations around the mean. The 95% band is simply the CAGR +/- two times the standard deviation, and the width is simply two times the standard deviation. As expected, we can conclude from the table that the strategy with the highest CV ratio also has the widest return confidence interval. In other words, the performance of the strategy is more volatile with annual returns varying more widely. The strategy with the lower CV ratio has a narrower return confidence interval and thus is more likely to achieve the backtested CAGR in any given year.

If you’d like to calculate the confidence band of your portfolio simply subtract two times the annual standard deviation from the CAGR for the lower bound and add two times the annual standard deviation to the CAGR for the upper bound. The computed range provides you with a 95% confidence interval of future returns. (As an aside, this is a crude calculation that provides a quick estimate. One should really use the arithmetic mean and confidence intervals assume normal distribution which may not be the case.)

The CV ratio is a powerful way to build portfolios providing many desirable attributes, both in terms of performance and trader psychology. We believe that the vast majority of traders are best served trading portfolios that are optimsed for consistency. Quantlab makes it easy to build, test and trade consistent portfolios.

Happy Trading,

PJ

3 comments On CAGR Confidence Intervals and Consistency

Oh my goodness! Impressive article dude! Thank you, However I am experiencing issues with your RSS. I don’t know the reason why I can’t subscribe to it. Is there anybody having similar RSS issues? Anybody who knows the answer will you kindly respond? Thanks!!

Hi, thanks for your message. Not exactly sure what’s up with the RSS feed. We’re using the default rss feed and appears to be in order. Will investigate and report back. Thanks.

Awsome blog! I am loving it!! Will be back later to read some more. I am bookmarking your feeds also.