Last week we explored the “best-day-of-the-week” theory and found no significant evidence to suggest that there is an optimal day of the week to trade. This week I’m going to test the theory that there is an optimal time of month to trade, and as you shall soon learn, things …

Blog Posts

In my post “Engineering a Synthetic Volatility Index” I discussed a technique that I’ve developed to monitor broad market volatility with a Synthetic Volatility Index. Today I’m going to quantify our index by applying it to a liquid universe of equities as a simple entry filter. If volatility indeed has an …

I employ volatility analysis extensively in the hedge fund I manage both at the individual stock level and at the index level. Both types of analysis are essential if you hope to trade successfully, so in today’s blog I’m going to discuss each of them. Index volatility will however form …

Last year Rowan spoke about the importance of consistency in portfolio construction and today I’d like to expand on the concept a little. There are a number of reasons why consistency is important: 1) our performance pegged pricing structure is based on consistency 2) it’s psychologically easier to trade consistent …

Trading is difficult because we’re all burdened with emotional challenges. It doesn’t matter how effective your strategy or statistically significant your testing, every strategy will experience drawdown and losing runs. It’s how we respond to those inevitable losses that determines whether or not we’ll be successful in the long-term. In …

I’ve been doing some research around something called External Relative Strength (ERS). ERS measures the stock’s price performance relative to all other listed equities. Basically, it measures how well or poorly a stock is performing relative to its’ peers. Our research suggests that the market has a strong propensity to …

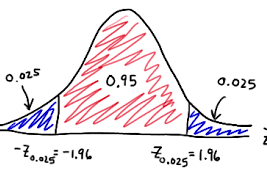

Few propositions in economics are held with more fervour than the view that financial markets are “efficient”, or that future price changes are unpredictable. Another strongly held view is the random walk hypothesis, which state that stock prices evolve according to a random walk and thus cannot be predicted. If …

After my blog last week on ANG the stock rose dramatically on an intraday basis, almost 9%! Many of our clients with long positions in the stock managed to close out near the highs, recouping most of their losses. I had someone ask what I thought caused the spike higher, …

In their excellent paper, Cole Wilcox and Eric Crittenden explore whether or not trend following strategies can achieve alpha when applied to the stock market. The vast majority of funds that operate trend following type strategies focus in the commodity and forex markets, where long-term sustainable trends driven by economic …

In this post I’ll review a simple strategy that I developed many years ago that attempts to exploit reversion to the mean. I’ve named the strategy Jaws due to the Jaw like pattern that the indicators exhibit before an entry condition occurs. The rules: Buy on the close when the …